shinyapp-basicusage-alphavantagepf

Source:vignettes/shinyapp-alphavantagepf.Rmd

shinyapp-alphavantagepf.RmdThe Alphavantagepf package also contains a Shiny Application which can be used to query, save, and visualize basic market information without having to navigate the asset-specific functions provided by the Alphavantage API. The app provides an intuitive way to compare small baskets of assets both technically and fundamentally.

This vignette will first go through some overall design goals and conventions before providing an overview of how to start and configure the application. Once it is running, we then give a brief overview of list management and individual analysis components. Augmenting the data is also described. Future plans are discussed in an appendix.

Overall design goals and conventions

The app is designed to

- Integrate four of the main asset classes into the analysis. For example, an equity, an index and FX exchange rate can all be plotted together.

- Minimize the amount of price information downloaded by caching (to the degree possible) older price data.

- Provide interfaces for capturing any data requested and adding external data to the internal cache.

- Provide easy ways to create and retrieve baskets of assets.

- Use modern design elements as much as possible, in particular the gt package and the dygraphs package. The latter is used via a “sister” package FinanceGraphs

A few conventions which are helpful to know before using the app are

| Item | Convention | Example |

|---|---|---|

| Asset Sets | Semicolon ; delimited |

"IBM;NDX;USD/MXN" |

| Relative Dates | (Signed) integers followed by [m|d|y],

relative to today |

"-4m" |

| Date Ranges | Relative dates separated by "::"

|

"-4m::", "-1y::+1y"

|

App invocation and initial setup.

The app requires a very modest amount of setup before using. It can be run with

require(alphavantagepf)

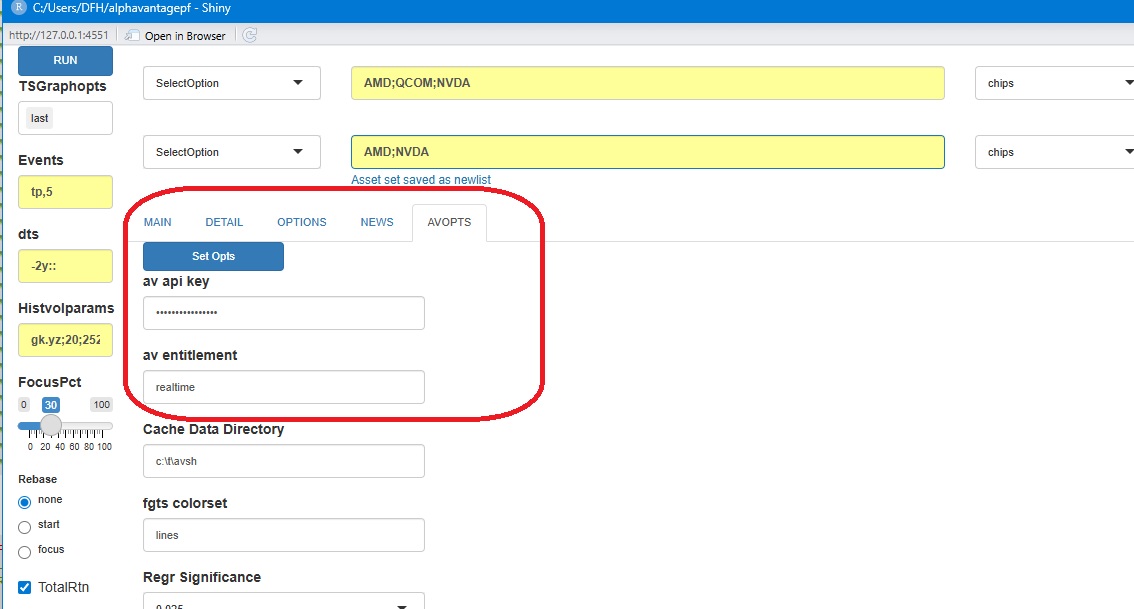

#> Loading required package: alphavantagepfWhen the app is first run, the following screen will be shown, with

the AVOPTS tab

selected. The first order of business will be to set the Alphavantage

API keys. To do so, just type or copy in both your API key and your

entitlement status (Either delayed or

realtime), and hit the blue Set Opts

button.

Other optional items that can be set are

| Item | Description |

|---|---|

| Cache Data Directory | Directory to store cached price data. If not specified, a temporary directory will be created and used. |

| Cached data is in a price file (in fst format), and an inventory file | |

| fgts colorset | A named aesthetic set for time series line colors, See fg_update_aes() |

| Regr Significance | p-values below which regression terms will be highlighted |

| AV dump directory | A directory in which to create a file with each downloaded function call. See below for details. |

| Capture AV Data | What Alphavantage calls to capture (e.g. Prices, non-prices, or all data) |

| Update or Cumulative | If Update, then captured data will be

keyed and updated only if new, otherwise all data captured |

For example, Update will only store the

latest price for a particular symbol and date |

|

| Data Saving Options | Control how often the captured data file is cleared or saved |

When capturing is turned on, a file called

av_download.RD will be created and updated in the specified

dump directory. This file will be a named list of data.tables, with a

data.table containing all downloaded data corresponding to an

Alphavantage function (e.g. TIME_SERIES_DAILY). If

“cumulative” is selected, all data will time-stamped and added to the

relevant data.table. If not, then data will be replaced for each

relevant key (usually SYMBOL). The user can then use that

file to integrate search histories into other analytics, such as a

rolling Markdown file.

Asset List management

Securities are seldom analyzed in isolation. It is easy to create and use ad-hoc groups of securities in this app.

To create a list, First, type in a new name for the list in the list box as shown below, and Hit Enter. Second, type in the components (separated by semi-colons) and hit the set button.

To get the assets in a list, select the desired list from the dropdown and hit get button.

You can see a table of current asset lists by running the “Gen:Inventory” command, and can add asset lists outside of the app using av_add_assetgroups()

Running Basic Analyses

To run analyses, select the desired item from the dropdowns and press the blue RUN button. One of more graphs or tables will be shown in the MAIN tab, with additional data possible in the DETAIL tab. That tab (the one to the right of MAIN) will change headings when relevant.

Graph events and decorations can be specified in the first two boxes,

with annotations for the last level and 5 turning points used as

defaults. The options possible are detailed in the fgts_dygraph()

documentation. Empty out the boxes for clean graphs. The date ranges

plotted come from the “dts” box (see above for conventions), and more

recent data can be focused in on using the FocusPct slider. For example, if the slider is

set to 50pct, and the date string is "-2y::" then the graph

will only show the last year of data, but can be slid back to see the

entire 2 year period.

Note that status messages are sent to the console if the “Status Msgs” box is checked and output data for each analysis is copied to the clipboad if the “copyTable” box is checked.

Plotting options

Data is plotted in raw form unless the Rebase options are used. Rebasing at the start will normalize all series to 100 at the start of the window. (In the the example above, the rebase would occur at the first point plotted 2 years prior to today). If Rebasing is set to the focus point, the rebasing occurs at that point set by the slider.

An alternative to rebasing is to plot the first asset on its own

axis, which can be done by selecting "splitts" in the

"TSGraphOpts" box. Other options that can be selected in

that box are

- Highlighting the first series with a thicker line

- Adding Labels showing the last value or series title

- Adding hi-low shading, if the data is available.

- Changing the line colors (via the

"fgts colorset"setting in the AVOPTS tab.)

Event codes can also be specified in the "events" box.

See fg_get_dates_of_interest()

and Dygraphs

vignette These can be single day events or highlighted ranges of

dates. (An example is below.)

Time series graphs are harder to interpret when muitple time series

frequencies or missing data is plotted together.

When time series do not appear to be daily, they will be plotted with

step functions. When data is missing (as would be the case when plotting

equities with assets such as FX or Crypto that trade over weekends),

gaps in the time series will be evident.

Analyses that can be run

The table below shows the current analyses that can be run. Select what you wish and hit the RUN button.

| Analysis | Explanation/Notes |

|---|---|

| Gen:Inventory | Price inventory and Asset Lists |

| Gen:LivePx | Live Price Table |

| Gen:NameSearch | Search for an Equity or Index [1] |

| TS:PriceTS | Time Series of Prices [2],[3] |

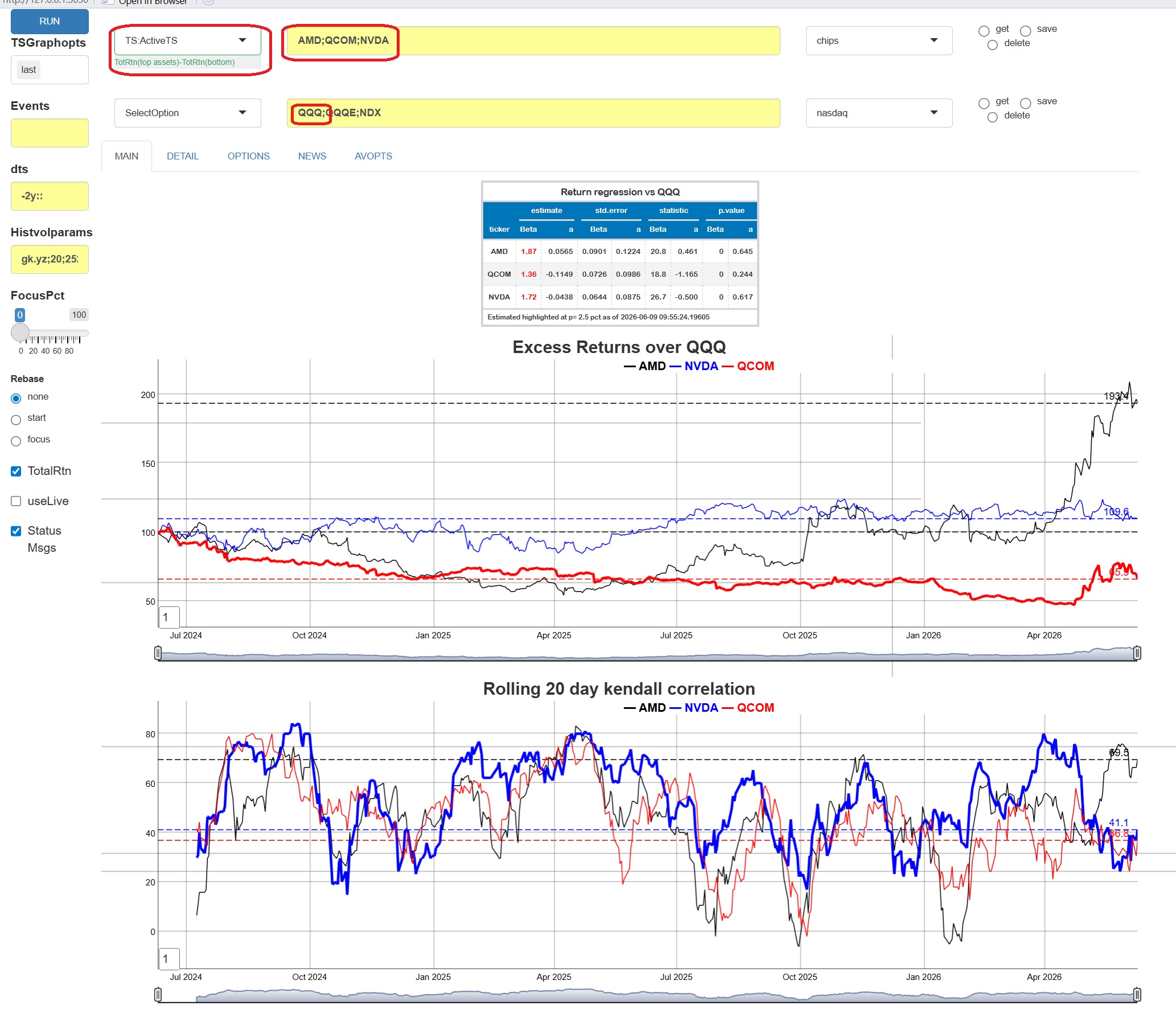

| TS:ActiveTS | Time Series of Total Return of Line 1 Assets less Line 2 [4] |

| TS:HistVolTS | Time series of Rolling volatilities and correlations [5] |

| EQ:DES | Table of descriptive data for Line 1 Assets |

| EQ:News | Table of recent news items for Line 1 Assets [6] |

| EQ:DivEarn | Table of Dividends and Earnings for Line 1 Assets |

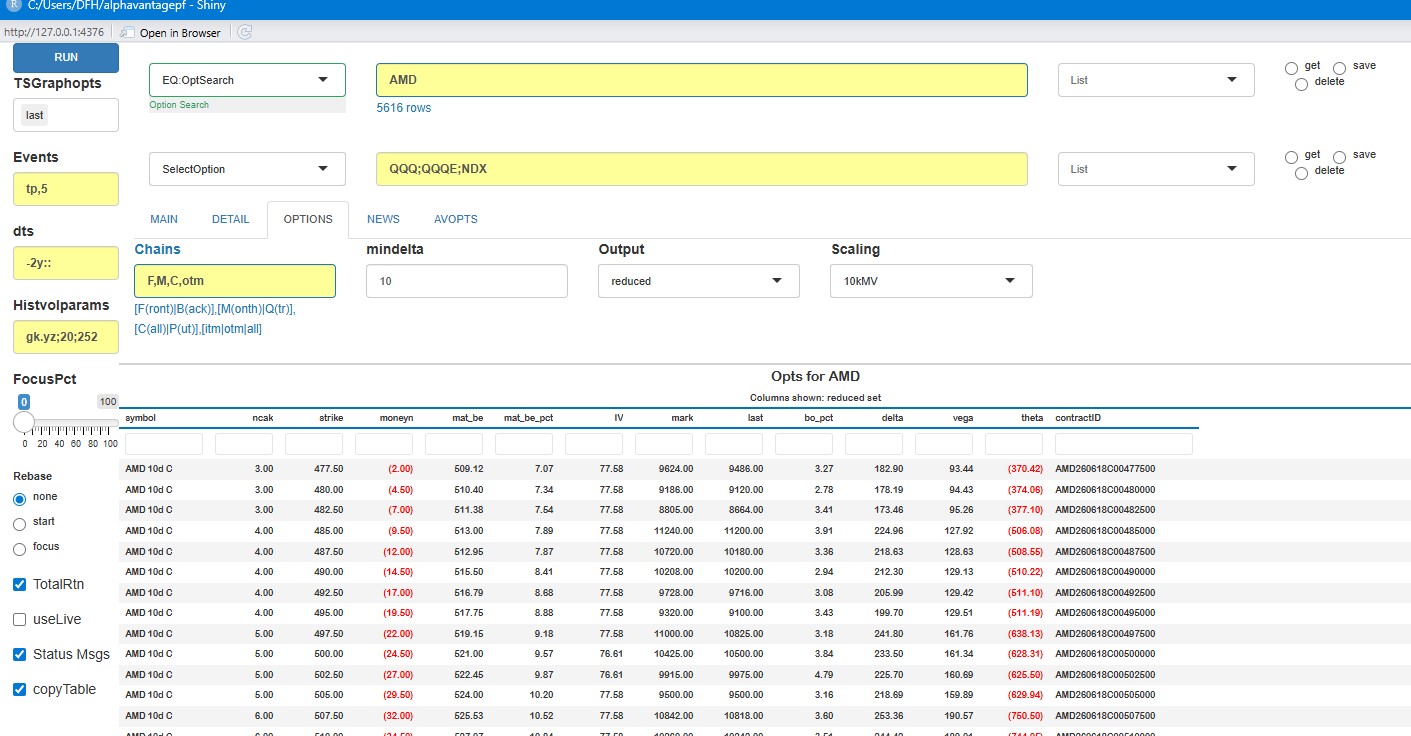

| EQ:OptSearch | Option Lookup and Search [7] (See Section Below) |

| Gen:Movers | US Market Movers |

Notes

1 Due to Alphavantage limitations, the search returns tickers that begin with the search term.

Graphing options are described above. THe graph can interactively be zoomed in on and reset with a double click.

Two synchronized graphs can be used by selecting this option for both Line 1 and Line 2.Total return data is used unless the box is unchecked. The data is augmented by live data if the box is checked.

Graphs show active returns, i.e. Total return of each asset in Line 1 less the first asset (typically a benchmark index) in Line 2. Rolling correlations and full period betas are also shown.

Volatilitity parameters in the Histvolparams box are passed to the [TTR::volatility()] function.

Results will be displayed in the OPTIONS tab.

Results will be displayed in the NEWS tab.

As an example, suppose we wish to look at active returns of three

popular chip manufacturers against the Nasdaq 100 broad index. Put the

tickers of interest in Line 1, and an index in Line 2. (If there are

more than one tickers in Line 2, only the first is used.) Select

TS:ActiveTS and hit run. The app will get whatever data it

needs, typically from the cache, but augmented with most recent (live)

data and produce the following output:

Here

is another example which highlights both the comprehensive abilities to

combine assets in the app with graphing abilities. Suppose we wish to

plot the fair value history of the crypto ETF

Here

is another example which highlights both the comprehensive abilities to

combine assets in the app with graphing abilities. Suppose we wish to

plot the fair value history of the crypto ETF IBIT, and add

some visual indication of overall market direction. Using the

TS:ActiveTS analysis with IBIT on line 1,

BTC/USD on line 2, and doi:regm in Events, we

would see

Option Search

To find options for a given set of tickers, Run “EQ:Optsearch” which will take you to the OPTIONS tab. A few fields on that page which will help narrow down the options are:

| Field | Detail |

|---|---|

| Chains | Comma delimited string of four items to narrow downloaded options. |

1. [F|B] first contract or second

contract |

|

2. [M|Q] Monthly expiration or Quarterly

expiration |

|

3. [C|P|A] Calls, Puts or Both |

|

4. [itm|otm|all] In or out of the

money |

|

| Mindelta | Minimum absolute delta of option |

| Output | Subset of columns to show, relevant to Trading or Valuation |

| Scaling | Values and Greeks for 10 contracts or 10kUSD premium |

The app looks up the current spot to determine moneyness. A skew graph is plotted after the table.

Managing data outside of the app.

The Shiny App also has facilities for adding and retrieving time

series data externally using other R scripts or documents. All of the

downloaded price history, as well as an inventory of prices are stored

either in a temporary directory created when the app is first run, or a

directory specified in the "AVOPTS" tab. The price data is

stored in fst format, which

has been the performance winner for several years. Time series data

stored in that cache augments that returned by (e.g.)

av_get_pf("IBM","TIME_SERIES_DAILY") function wih split and

dividend data returned by other av_get_pf()

calls. The full set is shown below. Note that a timestamp for each data

retrieval is also kept.

symbol timestamp open high low close adjusted_close dividend_amount split_coefficient ts origclose

<char> <IDat> <num> <num> <num> <num> <num> <num> <num> <POSc> <num>

ABBNY 2001-04-06 7.37 7.37 7.27 7.29 7.29 0 0.433 2026-05-31 08:06:48 16.8

ABBNY 2001-04-09 7.32 7.50 7.32 7.50 7.50 0 0.433 2026-05-31 08:06:48 17.3Adding data and integrating different asset classes.

The data can also be added to externally using the [av_add_data()] function. Any time series can be added, but not all time series can be guaranteed to be updated by Alphavantage calls. One difficulty with Alphavantages’ API platform is that there are different function calls (and returned data sets) for each major asset class. This app integrates them into one price table, but at the expense of having to know each asset type for the data added.

The app tries to determine what asset class a symbol is to update it

using av_get_pf()

calls as best as it can. Specifically, each new ticker is checked

against current Index lists, cryptocurrency lists, and then with

Alphavantage’s "SYMBOL_SEARCH". If several tickers

are passed at once, this can be quite expensive, as

Alphavantage tends to limit data usage if too many calls are made in

succession. If possible, it’s much better to predetermine the asset type

(one of c("Equity","ETF","Index","FX","Crypto")) in advance

and pass it to [av_add_data()] call at runtime.

Data which is completely exogenous to Alphavantage can also be added

to the cached data set. If the asset type isn’t specified or cannot be

determined, it’s assumed to be a "user" asset type which

isn’t updated, but can still be plotted or used. As an example, suppose

we wish to plot the prices of a common credit ETF against FRED’s

FEDFUNDS data. We will download both and add them programmatically.

Generic data needs to be manipulated into the form the app expects, but

data downloaded from Alphavantage is already in that form.

# av_add_data can be used simply, but

av_add_data(av_get_pf("IBM","TIME_SERIES_DAILY_ADJUSTED"))

# For many assets, use this

asset_df <- data.frame(symbol=c("HYG"),type=c("ETF"),currency=c("USD"), name=c("HY ETF"))

av_add_data(av_get_pf("HYG","TIME_SERIES_DAILY_ADJUSTED"), assettypes=asset_df)

# External Data

suppressMessages(require(quantmod))

ffdta <- as.data.table(quantmod::getSymbols("FEDFUNDS",src="FRED",auto.assign=FALSE))

ffdta <- ffdta[,.(DT_ENTRY=index,close=FEDFUNDS,adjusted_close=FEDFUNDS,symbol="FEDFUNDS")]

av_add_data(ffdta)

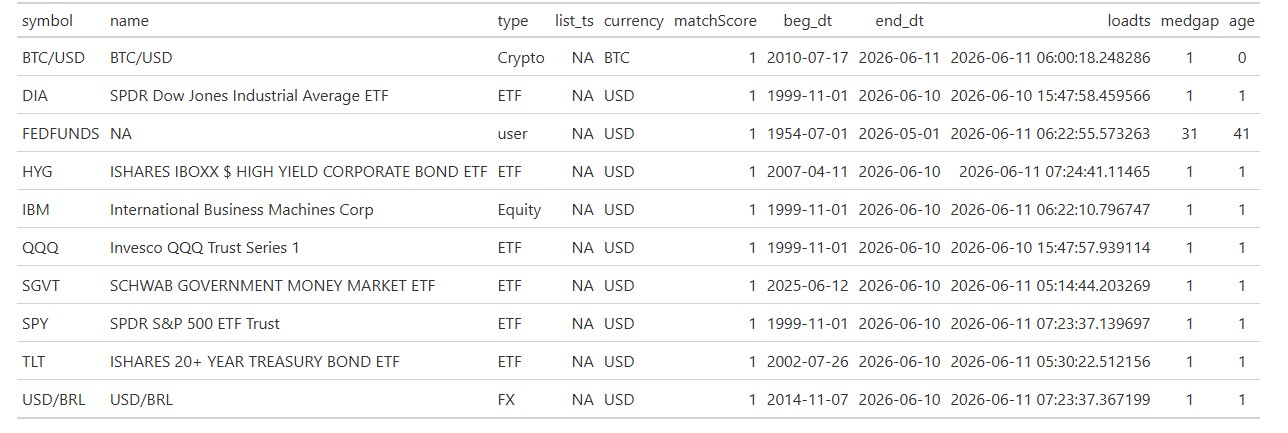

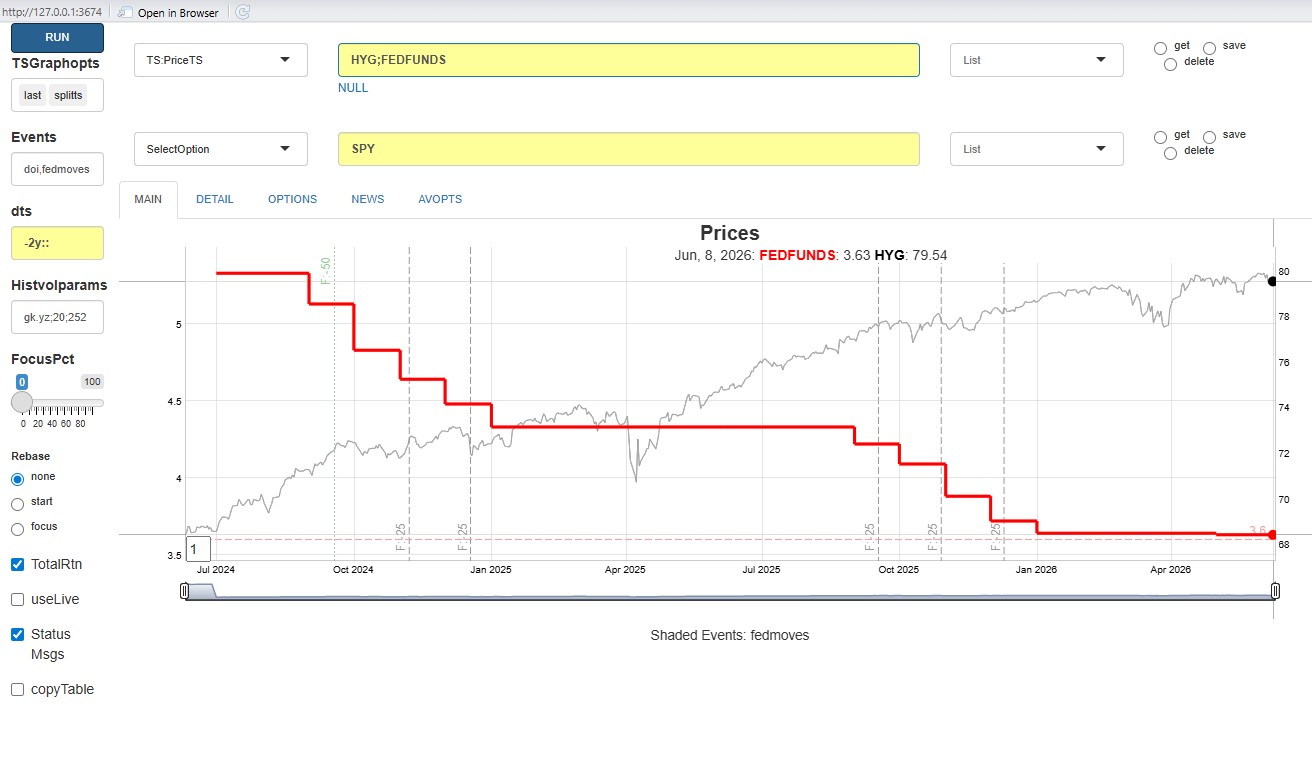

dump_inv() |> gt() The

data added can be plotted using the

The

data added can be plotted using the "TS:PriceTS" analytic,

as seen below. Note that the monthly time series needs to be used with

care, since it doesn’t correspond to the actual Fed Meetings.

Future plans

Planned improvements currently include

- Earnings and dividends incorporated into plots

- Ability to plug in user-defined functions which have access to the internal data store.

- Correlation and hedging analyses.

- Calendars

- Interface to events and aesthetics sets relevant to FinanceGraphs